The $70B Case for Getting CV & IR Revenue Right

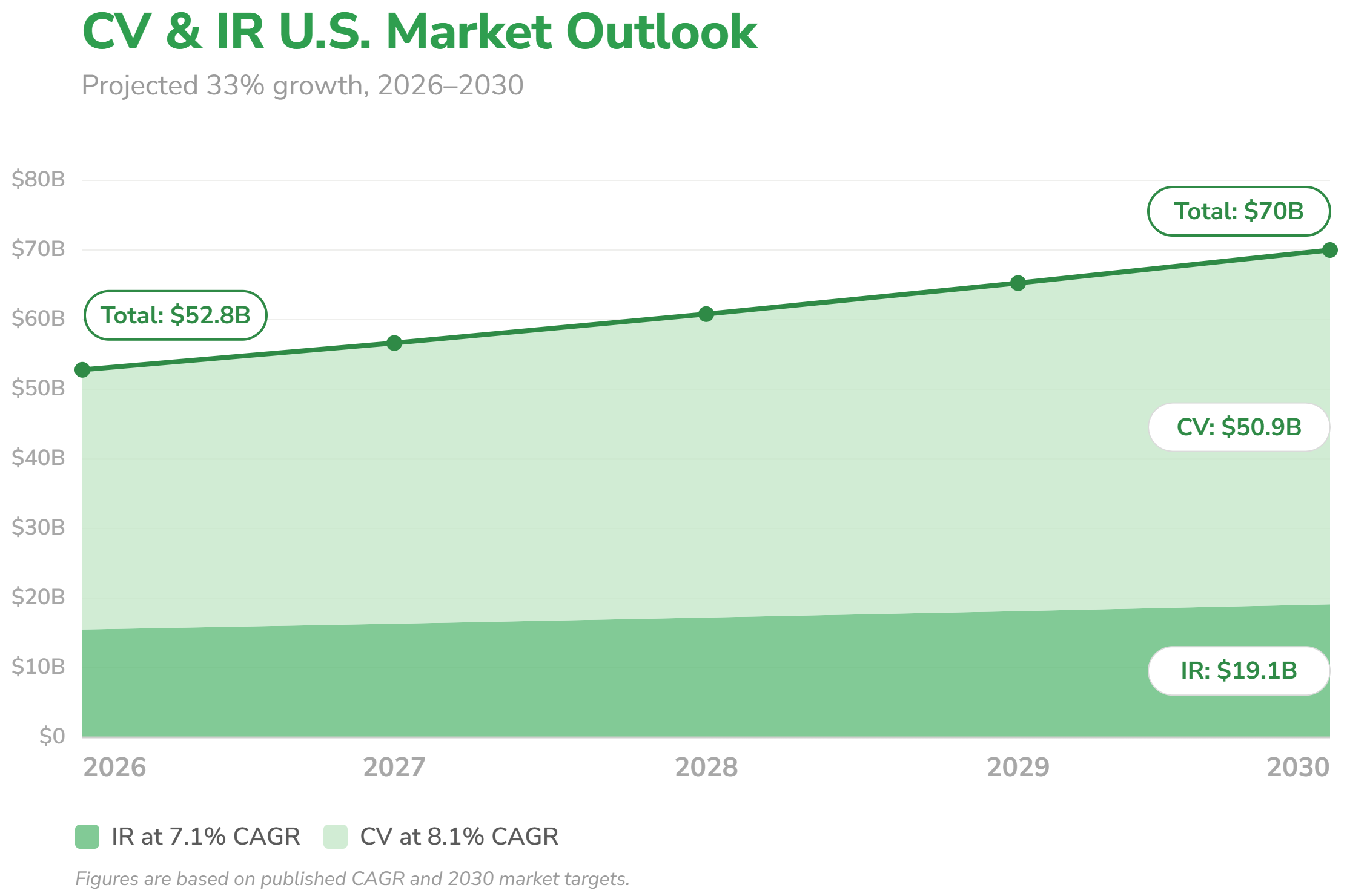

Interventional cardiology and interventional radiology are two of the fastest-growing service lines in medicine. CV is growing at 8.1% annually, whereas IR is growing at 7.1%. The combined CV & IR U.S. market is projected to increase from $52.8 billion to $70 billion by 2030. That trajectory reflects a service line in the middle of a fundamental shift. The procedure landscape, the coding requirements, and the reimbursement environment are all changing. That growth represents a significant revenue opportunity, but only for programs whose documentation and coding can capture it.

A Rapidly Expanding Procedure Landscape

Hospital service lines are shifting away from open surgery toward minimally invasive, image-guided procedures. Shorter recovery times, fewer complications, lower infection rates, and reduced hospital stays are pulling physician preference and patient demand in the same direction. That shift is not just a clinical story: more eligible patients means more volume, more complexity, and more revenue at risk if documentation and coding don't keep pace.

Four forces are reshaping CV & IR, each bringing its own documentation requirements and revenue at stake: structural heart caseload is expanding as indications broaden to lower-risk patients, IR is moving into new clinical territory beyond vascular disease, outpatient settings are capturing cases that once lived exclusively in hospital cath labs, and CMS reimbursement policy is actively incentivizing that migration.

TAVR generated nearly $7 billion globally in 2024, and the trajectory is accelerating. In June, CMS proposed extending Medicare coverage to asymptomatic severe aortic stenosis patients, a group that has historically been excluded from treatment despite representing a significant share of severe AS diagnoses. The proposal also removes hospital volume and operator requirements for new TAVR programs, opening the door for more sites to start or scale a program.

IR's procedure library is expanding too: prostatic artery embolization for BPH, genicular artery embolization for knee osteoarthritis, neuroembolization for subdural hematoma, liver ablation replacing resection in select cancer patients, and portal vein recanalization. Most of these cases once belonged to a different specialist entirely.

At the same time, the settings where CV & IR procedures are performed are growing between 8.1-11.2% CAGR. Reimbursement parity and patient access have made office-based labs and ASCs a genuine alternative to the hospital cath lab for a growing range of procedures. For OBL and ASC programs, that growth brings new documentation demands as procedure caseload expands. For hospital-based programs, the outpatient shift makes capturing every billable code on the cases that remain more critical than ever.

The Cost Of Getting It Wrong Is Higher Than Ever

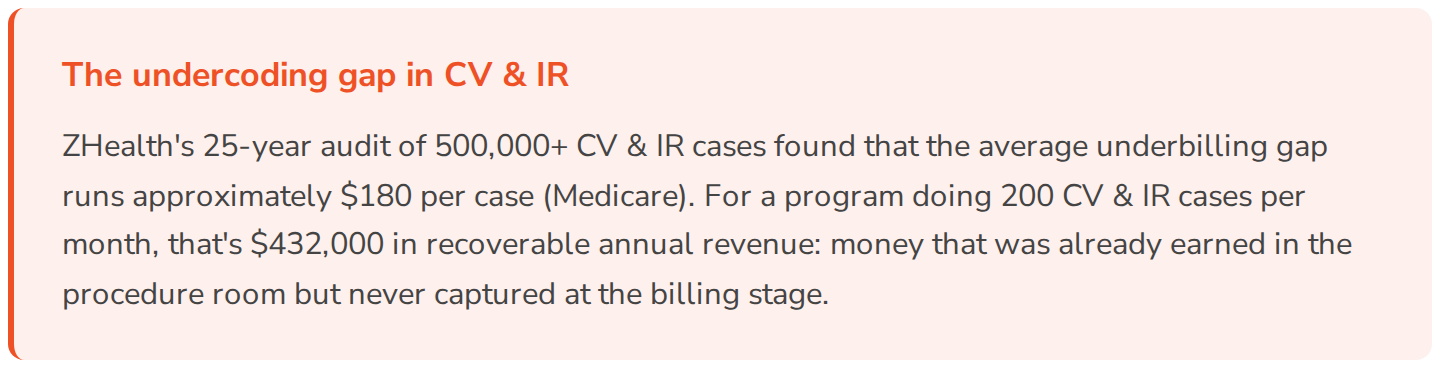

CV & IR cases generate substantial revenue for both hospitals and providers. Whether that revenue is fully captured depends on what happens after the patient leaves the procedure room. In a growing $70 billion market, the cumulative value of what gets lost in that journey is significant.

The operational reality makes it worse. The 2026 CMS fee schedule reduces facility-based practice expense allocations by 50% for hospital-based CV & IR procedures including TAVR, PCI, and ablation. Coding teams are stretched at the same time as case volumes climb and procedures become more complex. When documentation is incomplete, coders struggle to close cases cleanly, and queries delay billing by days or weeks. Undercoded claims leave revenue on the table, whereas overcoded claims create repayment liability and compliance exposure that may not surface until an audit. The OIG has already expressed interest in expanding audits for peripheral vascular procedures, which makes clean documentation more important than ever.

The programs that pull ahead in this market won't do so by seeing more cases alone. They'll do it by capturing more of the revenue those cases already generate. That means building documentation and coding accuracy into the clinical workflow before the case leaves the procedure room, not chasing it through the billing cycle afterward.

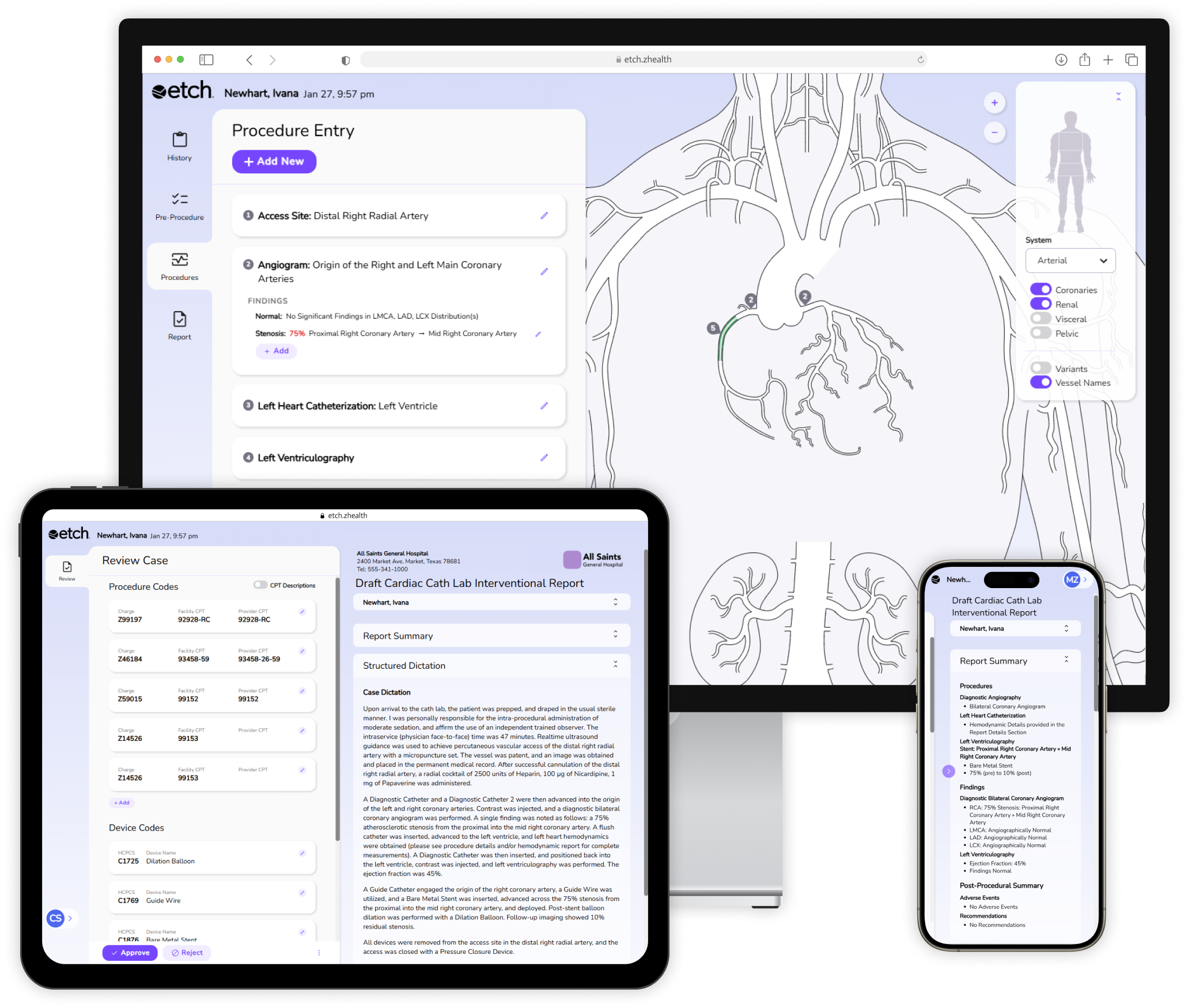

The Etch Effect

Here at ZHealth Documentation, we've built Etch software specifically for the growth and coding demands CV & IR programs are facing right now. As physicians document, Etch guides them through the specific clinical details that determine code assignment. Once documentation is complete, Etch automatically generates the codes in real-time with near 100% accuracy. With reimbursement rates shrinking, that accuracy matters more than ever: Etch helps programs capture the revenue they've already earned, without adding work to the clinical workflow.

References

Grand View Research. U.S. Cardiology Procedures Market Size, Share & Trends Analysis Report. Grand View Research, 2024, grandviewresearch.com

Grand View Research. U.S. Office-based Labs Market (2025 - 2033), 2025, grandviewresearch.com

Grand View Research. U.S. Ambulatory Surgery Center Market (2026 - 2033), 2026, grandviewresearch.com

Cardiovascular Business. CMS Proposes Major TAVR Changes, Including Medicare Coverage for symptomatic Patients, 2026, cardiovascularbusiness.com

Towards Healthcare. Interventional Radiology Market Grows with Rising Awareness of Non-Surgical Treatments, 2026, towardshealthcare.com

Global Market Insights. Interventional Radiology Market Size & Share 2026-2035, 2026, gminsights.com

Coherent Market Insights. Interventinal Radiology Market Analysis & Forecase: 2026-2033, 2026, coherentmarketinsights.com